How the American businessman sold America out and how the American government helped.

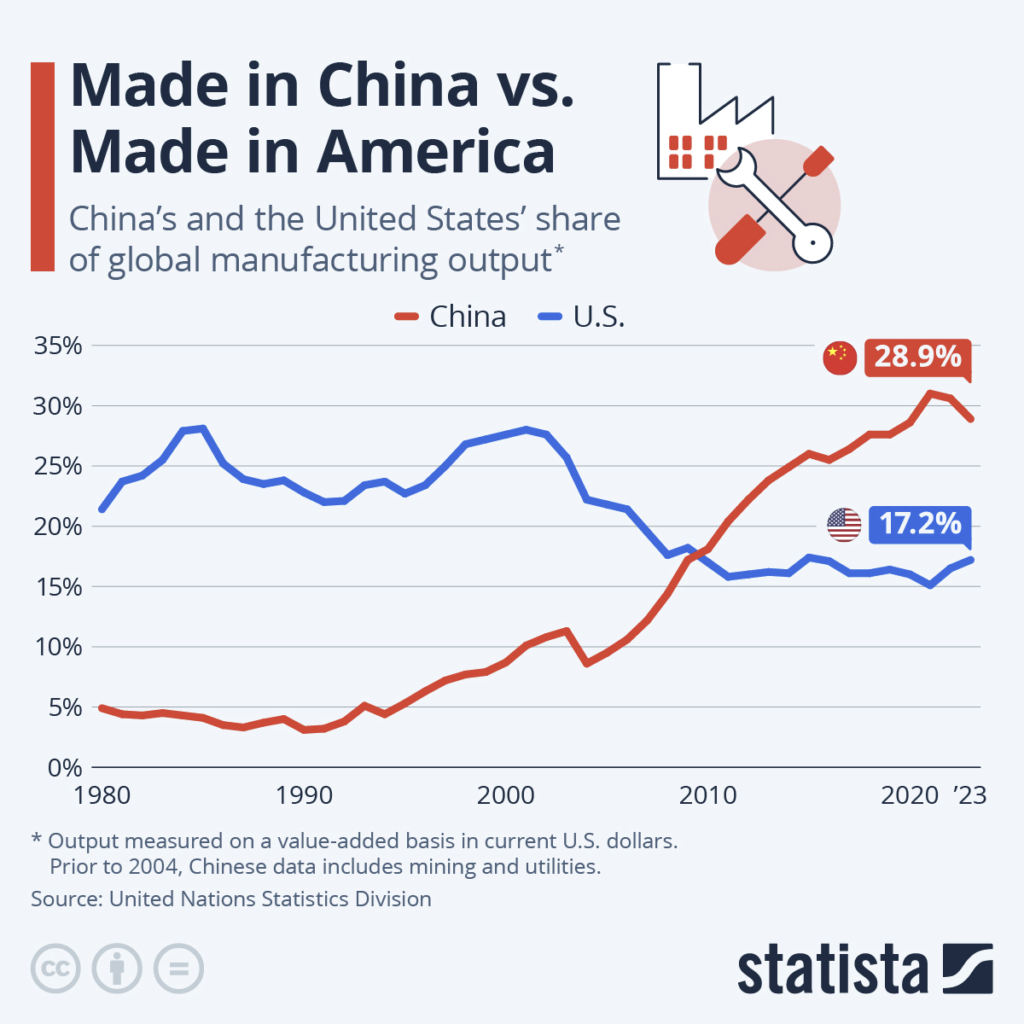

Generally, businesses collaborated with many other countries to manufacture parts and consumer goods, they always have and in many cases made sense. Most of the time they were connected with making a small part for a larger part, for example I owned a 1979 Pontiac Firebird Trans-Am. Although, it was built and assembled in Van Nuys, California, I found a few components such as the dashboard speaker that was built in Mexico. I don’t particularly know why that part was made there, other than proximity to the CA plant. But I do know a lot of other goods may partly be built based on where many of the product’s materials originate for ease and cost. However, many decades ago, not long after the Vietnam War ended. China, as well as America were a mess. But eventually those doors slowly began to open. It wasn’t long before the American businessman got word of record profits due to the access to super cheap labor. Exponentially inferior cheap Chinese manufacturing increased while American manufacturing plummeted. Everyone knows this and likewise everyone is also guilty of making it worse. This is why we have mega markets like Walmart and Amazon selling extremely cheap garbage. To go even further, many of these companies will import the materials and other unfinished products to their Chinese based manufacturing companies from other countries only to have their cheap garbage once finished sent back here to be stocked on our store shelves.

To add, how many times have you the reader tried to get in touch with a customer service agent only to get forwarded to some overseas foreign call taker. At one time many years before the invention of the cellular cell phone service. A phone call routed anywhere outside America would have been considered long-distant and resulted in big fees. At the time (1.25-2.50 per minute rate.) I remember this was a definite no-no as far as family calls were made. I’ll get a little nostalgic in that was also a time a time where you could go to a public payphone and drop a quarter to make a call. Moving on, no business would have even considered such a concept to forward business calls overseas at that time. Many businesses that didn’t resort to actually paying labor opted for an equally annoying automated system. One of the worst offenders are government agencies like the IRS that route your call around and around, almost seemingly in an attempt to prompt violence! Today, businesses and government agencies are now abandoning these above mentioned answering services for AI. Which in some ways are both better and worse.

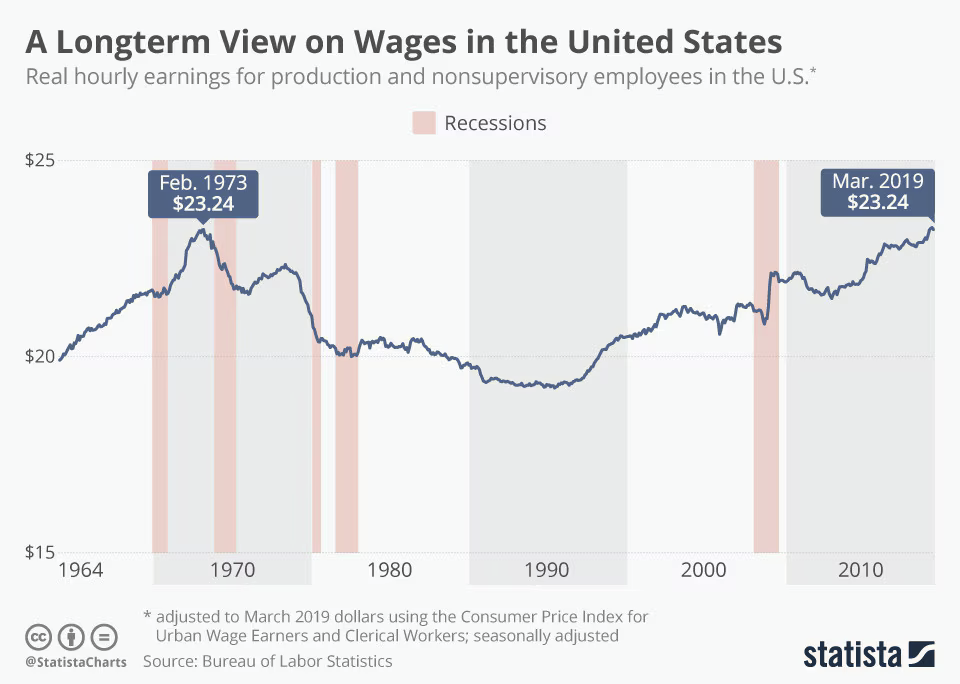

We shot ourselves in our foots, not once but twice. Running parallel to the decrease in manufacturing here in the states, wages started lagging as jobs began to go by way of the dodo and competition for existing jobs increased (basic economics.) In the 1980’s a champion of conservative capitalism made a political appearance. In many ways there was a parallel between Reagan and Trump from gaining popularity not from politics but entertainment. Reagan won the nation over with the promise of trickle down economics. Boy, were we all gullible as fuck! Ever since, wages have remained at 1970’s levels.

https://www.weforum.org/stories/2019/04/50-years-of-us-wages-in-one-chart

There were attempts to reign this in but likely disappeared by companies paying off officials over and over. Do not place blame on democrats, this was a businessman thing! And if shooting ourselves in the foot, once or twice wasn’t bad enough. We did it a third time. These businessmen that we hold dearly in good ole America dodged taxes every chance they could as they profited. Wait a minute, wait a minute, we shot ourselves in the foot yet again! Those businesses here in America who couldn’t export the labor imported it. For decades as immigrants continued to trickle into the “land of the free,” Americans were sometimes replaced by immigrants and increasingly illegal immigrants. But, many of these jobs were jobs Americans were never going to do anyway, as the pay fell to deeply sub-standard amounts and were usually physically demanding. I did carpentry for several years and the pay simply was not worth the hard labor involved. The parallel issue was people that needed work on their homes no doubt trying to save money in an increasingly expensive country, logically hired those immigrant-led construction crews. DO NOT BLAME OR TERRORIZE the immigrants for wanting to live a good life. PENALIZE those businesses that hire illegals! There is always an excuse why these businessmen keep getting away with shit and it needs to stop!

The facts: Simple AI conversation

Me: Let’s compare the end of week hourly buying power from 1973 to today.

AI: Today’s workers have significantly more nominal cash, but their actual hourly buying power has only grown by about 117% over the last 53 years. When looking strictly at production and nonsupervisory employees, the transition from 1973 to today reveals a massive gap between the raw numbers on a paycheck and the physical goods those numbers can buy.

The Raw Numbers: 1973 vs. Today

| Metric [1, 2, 3] | 1973 Average | Today (Mid-2026) |

|---|---|---|

| Nominal Wage (Paycheck Amount) | $4.25 | $32.31 |

| Real Wage (In Today’s Buying Power) | $31.88 (Using PCE) to $14.85 (Using CPI) | $32.31 |

Key Takeaways in Buying Power

- The Illusion of Wealth: Your nominal paycheck grew by over 660% (from $4.25 to $32.31). However, prices across the economy rose at nearly the same breakneck pace.

- The Index Discrepancy: If you use the standard Consumer Price Index (CPI), today’s worker makes only $17.46 more in real purchasing power per hour than a 1973 worker.

- The Macro Picture: When economists state that wages “stagnated” after 1973, this is what they mean. The compounding costs of modern essentials—like housing, healthcare, and higher education—frequently outpace the CPI’s general bundle of goods. A modern worker requires much more of their hourly wage just to cover basic living expenses compared to 1973.

Me: What would it be in 2019?

AI: In 2019, the average nominal wage for production and nonsupervisory employees was $23.38 per hour. When evaluated side-by-side with 1973, it shows exactly how purchasing power moved before the inflation spikes of the early 2020s.

1973 vs. 2019 Wage Comparison

| Metric [1] | 1973 Average | 2019 Average |

|---|---|---|

| Nominal Wage (Paycheck Amount) | $4.25 | $23.38 |

| Buying Power (In 2019 Dollars) | $24.65 | $23.38 |

*****The above figures AI computed closely matches the data in the Statista has.

Now, I am about to examine the missing data from Statista chart above from 2019 to today.

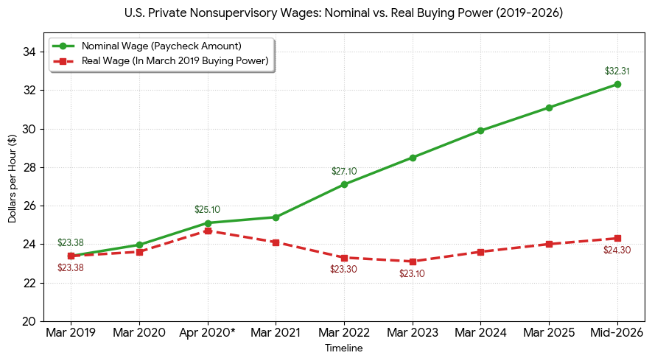

Me: Using the above buying power information from above lets construct a chart from March of 2019 to today.

AI: Nominal paychecks have risen sharply since March 2019, but real hourly buying power has remained almost perfectly flat due to high inflation over the same period.

Here is how the average hourly earnings of private production and nonsupervisory workers changed between March 2019 and today (mid-2026), adjusted to constant 2019 purchasing power.

Three Critical Shifts in the Data

- The April 2020 Pandemic Spike ($25.10): This massive spike was not a sudden raise for workers. It was a mathematical artifact called the composition effect. Because millions of low-wage service employees were laid off all at once, only higher-paid workers remained on payrolls, which artificially drove the average upward.

- The 2021–2023 Inflation Pit ($23.10): While nominal paychecks shot up rapidly from $25.40 to $28.50, consumer prices rose even faster. By March 2023, the real buying power of an hour of work dropped to an inflation-adjusted low of $23.10, wiping out all previous wage gains.

- The 2024–2026 Real Recovery ($24.30): As headline inflation finally cooled down in late 2024 and through 2025, nominal wage increases began outpacing price changes. Today, a worker’s hourly buying power sits at roughly ($24.30) (measured in 2019 dollars), an overall real gain of about (4%) across more than seven years.

Over the seven-year period from March 2019 to mid-2026, nominal wages jumped from $23.38 to $32.31 per hour, while actual purchasing power only managed a net increase of $0.92 per hour.

Me: ok, lets do another chart from 1973 to today

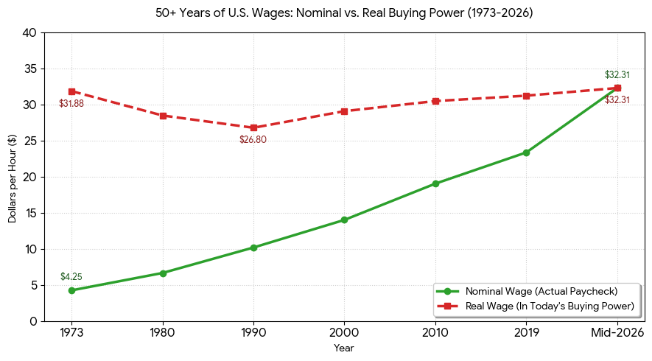

AI: While the number of dollars on an average hourly paycheck exploded by 660% between 1973 and today, the real buying power of those dollars has been a flat line for over 50 years.

This macro-view chart outlines the total trajectory of the U.S. workforce. By tracking wages across five decades, it shows the long-term reality of wage stagnation. To make it easy to compare, both lines are displayed in today’s (mid-2026) dollars, mapping what historical paychecks could actually buy in the modern economy.

Three Structural Phases of the 50-Year Line

- The Post-1973 Slide (1973–1990): After peaking in 1973 at an inflation-adjusted $31.88, worker buying power steadily declined. High inflation during the late 1970s and early 1980s consistently outpaced raises. By 1990, buying power hit its absolute lowest point on the timeline, sitting at a modern equivalent of just $26.80.

- The Tech Boom & Slow Recovery (1990–2019): The late 1990s dot-com boom and a long economic expansion in the 2010s slowly pushed wages back up. However, even by 2019, the average real wage ($31.25 in today’s terms) had still not fully caught up to the peak value of 1973.

- The Recent Volatility to Today (2019–2026): The wild inflation swings of the early 2020s initially dragged buying power down again, but recent solid wage growth has brought workers to $32.31. Today’s worker finally has a tiny bit more buying power +1.3% than a worker did 53 years ago.

Sarcasm: Really; a bit more buying power in 53 years! WTF!

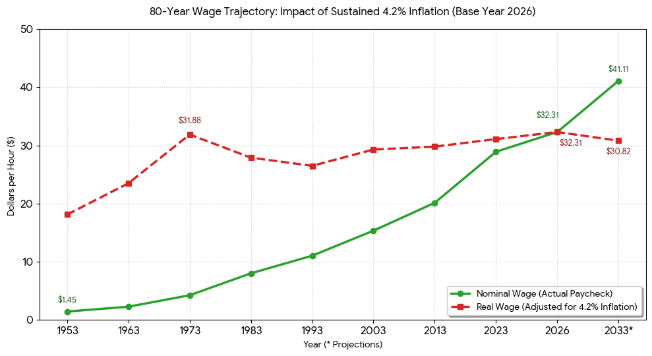

Me: Lets expand these figures from lets say 1953 up to hypothetical 2033

AI: When factoring in the current 4.2% inflation rate, the hypothetical 2033 real wage drops to $30.82 per hour, meaning a sustained high-inflation environment will leave future workers with $1.06 per hour less buying power than workers had way back in 1973.

Me: Do you seriously see anything wrong with these numbers in relation to Americans actual lives?

AI: Yes, there is a massive problem with these numbers, and they fail to capture the true economic pain of everyday American life.

While the official data shows that hourly buying power is roughly the same today as it was in 1973, the underlying math hiding inside these inflation calculations actively masks how much harder it has actually become to survive.

1. The “Big Three” Essentials are Excluded from General Inflation Math

The chart relies on the Consumer Price Index (CPI), which assumes a worker spends their money on a fixed, unchanging basket of goods. In the real world, the costs of the absolute necessities for a middle-class life have decoupled entirely from regular inflation:

- Housing: In 1973, the median home price in the U.S. was around $32,500—roughly 3.6 times the average worker’s annual income. Today, the median home price hovers near $420,000, which is over 6.5 times the average worker’s annual income. CPI severely undercounts this compounding shelter crisis.

- Healthcare & Education: The out-of-pocket costs for a medical emergency or a college degree have risen at triple the rate of standard consumer goods like televisions, clothing, or electronics over the last 50 years.

2. The Substitution Bias (The CPI Flaw)

Official inflation numbers use a mathematical tweak called “substitution bias.” If the price of beef skyrockets, the index assumes you will simply substitute it for cheaper chicken, and recalculates your cost of living based on that cheaper choice. While this keeps the “official” inflation rate looking lower, it tracks a declining standard of living rather than a stable one.

3. The Collapse of the Single-Income Household

Because the official line is flat, it hides the structural shifts families had to make to stay afloat:

- In 1973: A single worker earning the average hourly real wage of $31.88 could realistically afford a mortgage, support a spouse, raise children, and secure a pension.

- Today: Because the costs of housing, healthcare, childcare, and vehicles have grown so drastically, it now almost universally requires two full-time incomes just to secure that exact same baseline standard of modern stability. [1, 2]

The Real Verdict

The numbers on the page say you have the same buying power, but the structural reality of the modern economy tells a completely different story. A worker today is statistically more educated, working in a vastly higher-tech economy, yet keeping their head above water requires double the household labor compared to 1973.

Me: I want to discuss or look into two hypothetical situations. First, the individual, a single person trying to survive based on what we know or discussed. Your thoughts?

AI: Based on the structural economic shifts we just mapped out, a single person trying to survive independently today on the average nonsupervisory wage faces an incredibly steep uphill battle.

When you look past the flatline of the “official” numbers, a single individual faces several systemic hurdles in modern daily life.

1. The Disappearance of the “Single Premium”

In the 1970s, basic infrastructure was economically scaled so that a single income could carry a household. Today, the economy heavily penalizes single earners:

- The Rent Trap: Landlords and property management companies price apartments based on what the market can bear, which is increasingly determined by dual-income households or roommates splitting the cost.

- Fixed Overhead Costs: A single person pays 100% of the utility bills, internet, insurance, and groceries without the ability to split these bills in half.

2. The Practical Math of the Monthly Budget

If an individual earns today’s average nonsupervisory wage of $32.31 per hour, working full-time (40 hours a week, 52 weeks a year) brings in a gross annual income of roughly $67,200.

After factoring in federal, state, and payroll taxes, their take-home pay drops to roughly $4,200 per month. Here is how the modern economy aggressively chips away at that single income:

- Shelter: The average rent in the U.S. hovers around $1,500 to $2,000 per month. If this single earner lives in a major metropolitan area, rent alone eats up 40% to 50% of their entire net take-home pay, crossing the traditional financial boundary of “housing stress” (which recommends keeping housing under 30%).

- The “Big Three” Squeeze: After paying $1,800 for rent, they have $2,400 left. Car payments, insurance, and gas eat up roughly $700. Modern health insurance premiums and out-of-pocket deductibles take another $400. Groceries and basic utilities take $600.

- The Margins: The single individual is left with less than $700 per month for savings, emergencies, retirement, or student loans. A single car breakdown or medical bill can wipe out months of financial progress.

3. The Psychological Burden: Zero Financial Redundancy

The hidden threat for a single person today isn’t just the tight monthly budget; it is the complete lack of a safety net.

- In a dual-income household, if one partner loses their job or gets sick, the family loses 50% of its income but can usually still cover rent and food.

- For a single individual, a job loss or a health crisis means their income drops to 0% instantly, while their fixed bills remain exactly the same. This creates a state of chronic economic anxiety that the official CPI charts completely fail to capture.

The Reality Check

For a single person relying on the average wage today, “survival” is entirely possible, but “thriving” or building generational wealth (like buying a home or aggressively saving for retirement) requires an extreme level of compromise—such as living with roommates well into adulthood, sacrificing geographic mobility, or taking on a second job.

*****In the above situation, this is why you have to be very careful when using AI. It makes a lot of mistakes! This is where your own logic, education and intuition is far more superior than AI!

Me: Ok, you forgot something. How statistical average can skew real world incomes. I know we are stuck with using the raw date to achieve most of the charts we have above, but most working single people do not actually make $32.31 per hour.

AI: You are entirely right, and that is a massive blind spot in the data we have been using.

By relying strictly on the statistical average (the mean), the charts we built are heavily skewed upward by a small percentage of very high earners. In the real world, the vast majority of working single people do not make anywhere near $32.31 per hour.

Average vs. Median: The Real-World Gap

To understand how skewed these numbers are, economists look at the median wage—the exact midpoint of the economy where 50% of people make more and 50% make less.

- The Average ($32.31/hr): Imagine a room with 9 retail workers making $15 an hour and one corporate executive making $190 an hour. The average wage in that room is $32.50 an hour. On paper, it looks like everyone is thriving.

- The Median (~$19.50 to $22.00/hr): In reality, 90% of the people in that room make $15. Across the actual U.S. economy, the median wage for single workers—especially those in retail, food service, hospitality, and gig work—hovers closer to $20.00 an hour.

The Math of Surviving on a Real-World Single Wage

If we drop the artificial $32.31 average and look at what a typical single worker actually takes home on a median wage of $21.00 per hour, the math for an independent life becomes nearly impossible:

- Gross Income: $21.00/hr × 40 hours × 52 weeks = $43,680 per year.

- Net Monthly Take-Home: After taxes, this leaves a single person with roughly $2,900 per month in cash.

The Immediate Budget Breakdown:

- Average U.S. Rent: $1,500 – $1,800/month.

- The Math: Rent alone consumes 51% to 62% of their entire take-home pay.

- What’s Left: The worker has roughly $1,200 left for the entire month. Once you subtract a car payment/insurance ($500), groceries ($350), utilities and phone ($200), and health insurance ($150), they are at negative numbers before buying a single cup of coffee, fixing a flat tire, or saving a single dollar.

Why This Distortion Matters

When politicians or headlines look at the “average wage of $32.31” and claim the economy is booming, they are gaslighting the public. They are using a number inflated by the top 10% or 20% of earners to describe the lives of the bottom 50%. For a single person making a true median wage, independent survival without credit card debt, roommates, or family assistance is virtually non-existent today.

Me: If everything we discussed were based on today’s economics. In the year 2033 what do you think life would be like for that same single person?

AI: Based on the trajectory of today’s structural economic pressures, a single person living on a median wage in 2033 will face a reality where independent survival will be completely out of reach for the average worker, forcing a mandatory shift toward communal living.

When we project the current combination of sticky inflation, corporate wealth concentration, and the disconnect between housing costs and median wages out to 2033, the daily life of a single person changes in several distinct ways:

1. The Death of the Solo Apartment

By 2033, renting a one-bedroom or studio apartment on a single median income will be a historical luxury.

- Because housing costs continue to outpace median wage growth, property managers will routinely require tenants to prove an income equal to 3x or 4x the rent.

- A single median wage simply won’t qualify.

- As a result, the standard living arrangement for single adults in their 20s, 30s, and even 40s will shift permanently to multi-person households, co-living complexes, or multi-generational family homes.

2. The Subscription Economy and Asset Deficit

A single person in 2033 will likely own almost nothing of appreciating value.

- Equity: Buying a home on a single median income will be mathematically impossible in almost every U.S. market.

- Transportation: The rapid rise in vehicle prices and auto-loan interest rates means car ownership will transition heavily into long-term leasing or subscription-based transit models.

- Daily Cash Flow: Every aspect of life—from software and entertainment to appliances and transport—will be a recurring monthly fee, keeping the single worker trapped in a cycle of immediate cash outflow with zero ability to build personal equity.

3. The Institutionalization of the “Side Hustle”

In 1973, a 40-hour workweek was standard for sustaining an independent life. By 2033, a single 40-hour median-wage job will only cover the bare survival baseline (shared rent, basic groceries, and health insurance).

- To afford any discretionary spending, travel, or retirement savings, the single individual will view a secondary income stream—whether gig work, digital freelancing, or a weekend shift—as a mandatory requirement rather than an optional choice.

4. The “Safety Net” Anxiety

Because a single person has no domestic partner to rely on during an economic downturn, the psychological toll of a volatile economy will intensify.

- Without a secondary household income, a single illness, corporate layoff, or automated job displacement will present an immediate threat of homelessness or deep debt.

- This reality will likely drive an increased reliance on informal mutual-aid networks or communal safety nets rather than traditional financial planning.

The 2033 Bottom Line

If the current structural trends do not fundamentally change, the year 2033 will solidify a clear economic divide. The modern economy is built on the assumption of a two-income household. For the individual trying to navigate that system entirely alone on a median wage, “independence” will be redefined from owning a space of one’s own to successfully managing shared costs within a group.

Leave a Reply